The biggest financial headlines in 2022 have been about poor market performance amidst high inflation. This has led many investors to search for ways to protect the value of the savings from eroding under inflation. There are 3 primary ways to guard against rising prices as a US-based investor: 1) Invest in equities or equity-like securities, 2) Invest in I-bonds, or 3) Invest in TIPS. But first, what exactly is inflation?

I generated this text in part with OpenAI’s large-scale language-generation models. Upon generating draft language, I reviewed, edited, and revised the language to my own liking and I take ultimate responsibility for the content of this publication.

Inflation is the rate at which the prices of goods and services increase over time. In the United States, the Consumer Price Index (CPI) is the key measure of inflation. The CPI tracks a basket of common household goods and services for changes in prices over time. The Bureau of Labor Statistics releases CPI data monthly. It can be caused by a variety of factors, including economic growth, government spending, and supply and demand. It’s important to remember that this can have both positive and negative effects on the economy.

Pros and cons of rising prices

On the positive side, it can stimulate economic growth by encouraging consumer spending and investment. In addition, rising prices can help to reduce unemployment by making it easier for businesses to create jobs. Rising prices can also lead to higher wages for workers.

On the negative side, inflation can erode the value of savings and reduce purchasing power. In addition, inflation can lead to higher interest rates, which can discourage investment and slow economic growth.

Now that we have some understanding of what we’re dealing with, how can we protect our portfolios against it? When it comes to protecting a portfolio against inflation, there are three primary options: stocks, I-bonds, and TIPS securities. Each option has its own pros and cons.

Stocks

Stocks have historically been one of the best investments for protecting against inflation. They tend to outperform other asset classes in periods of high inflation. The reason for this is that companies are able to pass on higher costs to consumers, which results in higher profits. In addition, stocks offer the potential for capital gains, which can further offset the effects of inflation. However, stocks are also more volatile than other asset classes, which means that they can lose value in periods of stable prices.

I-Bonds

I-bonds are a type of government bond that is specifically designed to protect against inflation. The US Treasury issues them and the US government guarantees them. I-bonds offer a fixed rate of interest, plus an additional variable rate that is based on the current rate of inflation. This variable rate is reset every six months, which means that I-bonds offer immediate protection against inflation.

However, investors in I-bonds are partially locked in for 5 years. If the investor cashes in before the 5 year point, they will lose 3 months of interest. And investors are fully locked in for the first year. This can be problematic in times of declining inflation, where an investor may be locked into a lower yield than expected as the interest rate resets.

TIPS

TIPS securities are another type of government bond that is specifically designed to protect against inflation. They are issued by the US Treasury and are backed by the full faith and credit of the US government. TIPS offer a fixed rate of interest, plus an additional variable rate that is based on CPI. This variable rate resets every six months, which means that TIPS offer immediate protection against inflation. However, like I-bonds, TIPS have a low yield and are not suitable for investors who are looking for income.

Is inflation actually a problem right now?

Investors are acutely concerned about rising prices right now. However, I think part of this problem has become overstated. The efforts of the Federal Reserve have begun to slow month-over-month changes in prices. This means that prices are actually already returning to a normal path. However, the numbers reported in headlines are year-over-year numbers.

This causes the headline number to overstate the current level of inflation. Let’s look at a simple example. Let’s say the CPI index in November 2021 was 100. Then there was a one-time inflationary event in January 2022, which jumped the index up to 110. After that, the market returned to normal, and the inflation index stayed at 110 for the rest of 2022.

In this scenario, by November 2022, inflation would be completely gone, but the year-over-year CPI print would be 10% until December 2022. This is an example of confusion that can be caused by looking at levels versus changes.

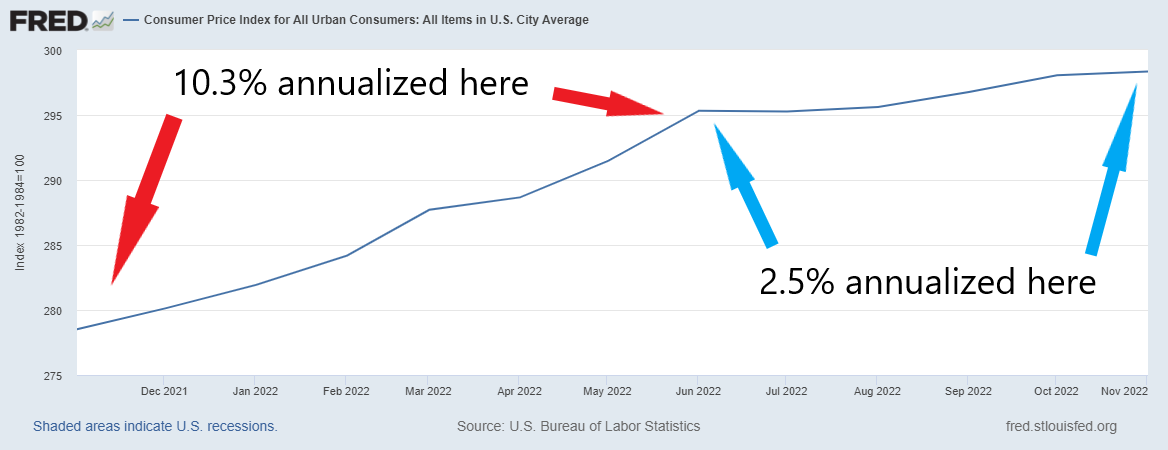

And in fact, the current real-world situation is actually a less-extreme version of this simple example. Let’s take a look at the level of the CPI index below:

Not bad for the past few months right?

Don’t miss out on future posts

Don’t miss any new posts! Sign up below to subscribe. I generally post once per month and I alternate between longer-form articles and short digests of interesting financial content from other sites I’ve found. Thanks for reading!

Discover more from Luther Wealth

Subscribe to get the latest posts sent to your email.